Polymarket Insider Trading and Federal Wire Fraud: What the Van Dyke Indictment Means

Posted on by Michael Lowe.

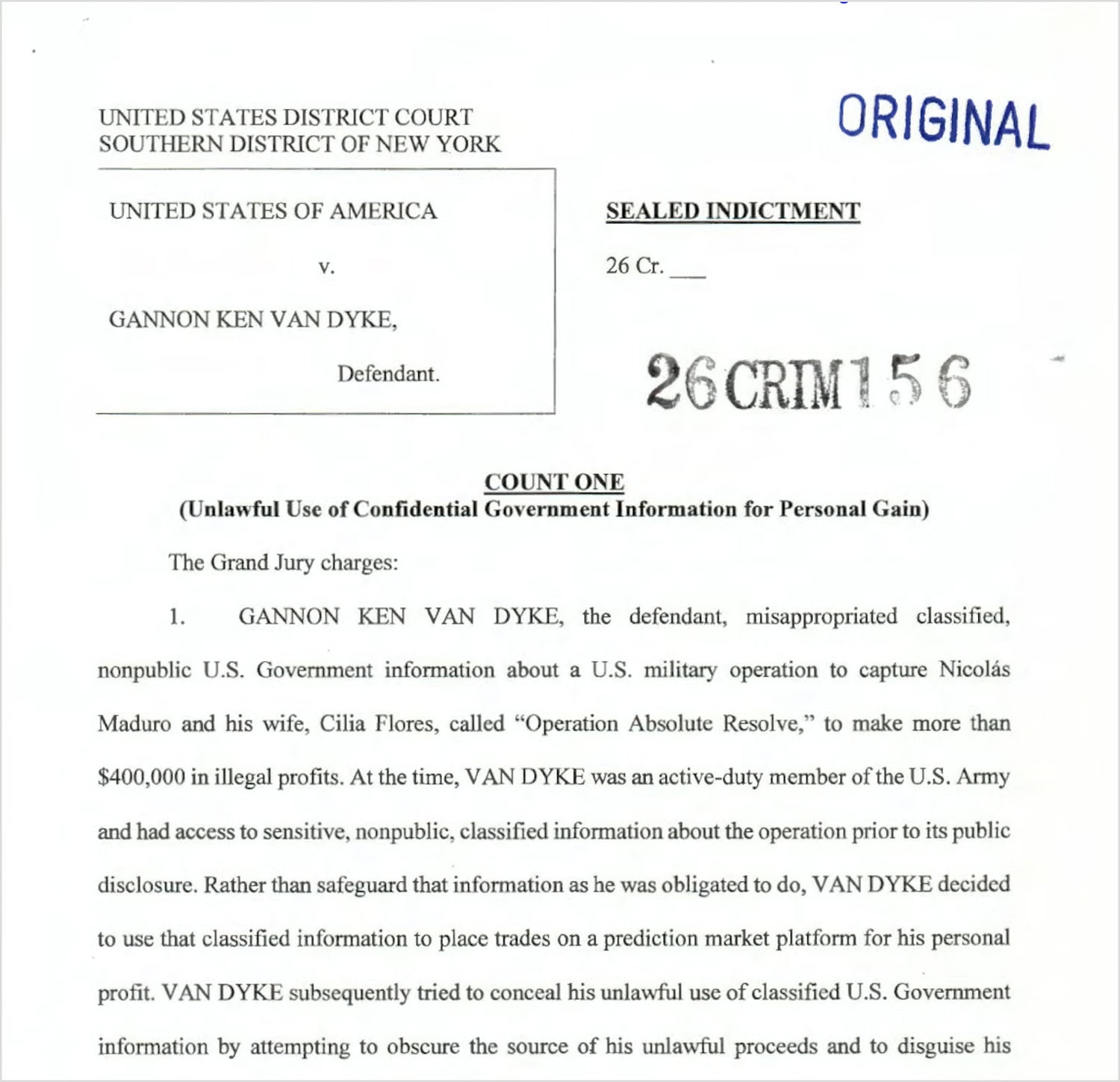

Polymarket insider trading just stopped being theoretical. On April 23, 2026, federal prosecutors in the Southern District of New York unsealed a five-count indictment that turned a U.S. Army Master Sergeant’s four-day Polymarket trading spree into a federal wire fraud and money laundering case, complete with a $404,000 forfeiture demand and the personal signature of Jay Clayton, the former Chairman of the Securities and Exchange Commission. If you have ever traded a Polymarket event contract on confidential information from your employer, your client, or any source you owed a duty to keep secret, the Van Dyke indictment is the prosecutorial template for what is coming. This article is written for you.

I am Michael Lowe. I have been a board certified criminal defense lawyer in Dallas for more than twenty-seven years. Before that I was a Dallas County felony prosecutor. I have tried more than 150 jury trials, the vast majority of them serious felonies including federal cases in the Northern and Eastern Districts of Texas. The analysis below is a federal defense lawyer’s read of what was charged in the Van Dyke case, why the same legal theories reach far beyond the defendant in that case, and what you should do right now if any of this is starting to sound personal.

The four days that ended a seventeen-year military career

Gannon Ken Van Dyke had been an active-duty soldier in the U.S. Army Special Forces since September 2008. By late 2025, as a Master Sergeant assigned to U.S. Army Special Operations Command at Fort Bragg, he was read into a classified operation called Operation Absolute Resolve. The plan was to capture Nicolas Maduro and his wife Cilia Flores and bring them to the United States to face drug trafficking conspiracy charges.

On December 8, 2025, Van Dyke received the standard Classified Information Security Briefing and signed an SF-312 Classified Information Nondisclosure Agreement. The form recited that he was being granted access to classified information and that, by signing, “special confidence and trust shall be placed in me by the United States Government.” He promised never to divulge any classified information to any unauthorized person.

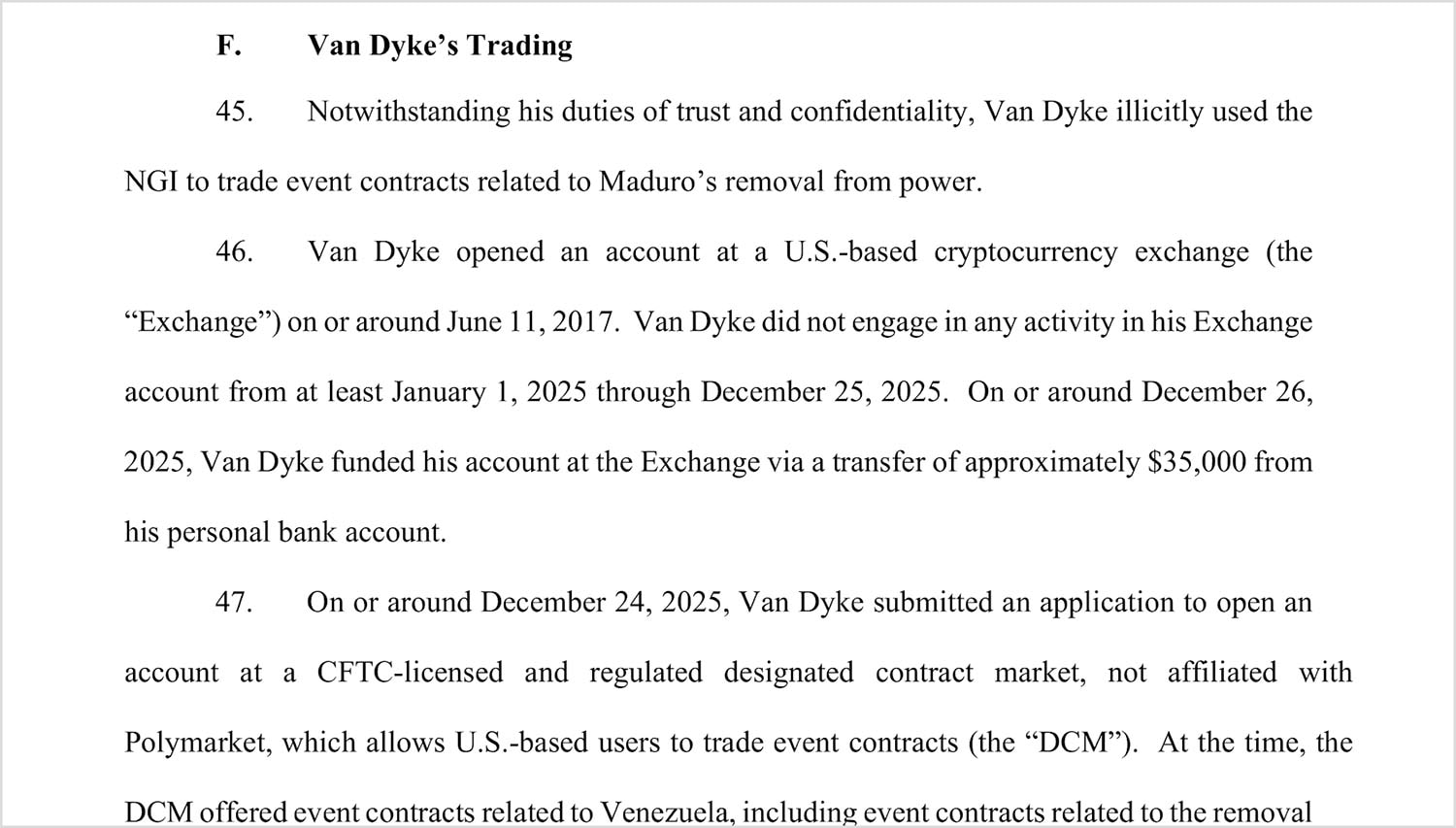

Eighteen days later, on December 26, 2025, Van Dyke reactivated a U.S.-based cryptocurrency exchange account that had sat completely dormant for the entire calendar year of 2025. He moved $35,000 of his own money into it, the first activity in that account in twelve months.

That same day, December 26, he tried to open an account at the only CFTC-licensed event-contract exchange where he could legally trade Maduro markets in the United States. Almost certainly Kalshi. Kalshi’s compliance system flagged him. He contacted Kalshi customer support on December 26, then again on December 27, then again on December 28, trying to get the rejection reversed. They would not let him in.

So he went to the unregulated DeFi side of Polymarket, where there is no know-your-customer check, no employer field, no government-employee flag. He created a new wallet at address 0x31a5…8ed9 and chose the handle “Burdensome-Mix.” He never used that wallet for anything else, before or after.

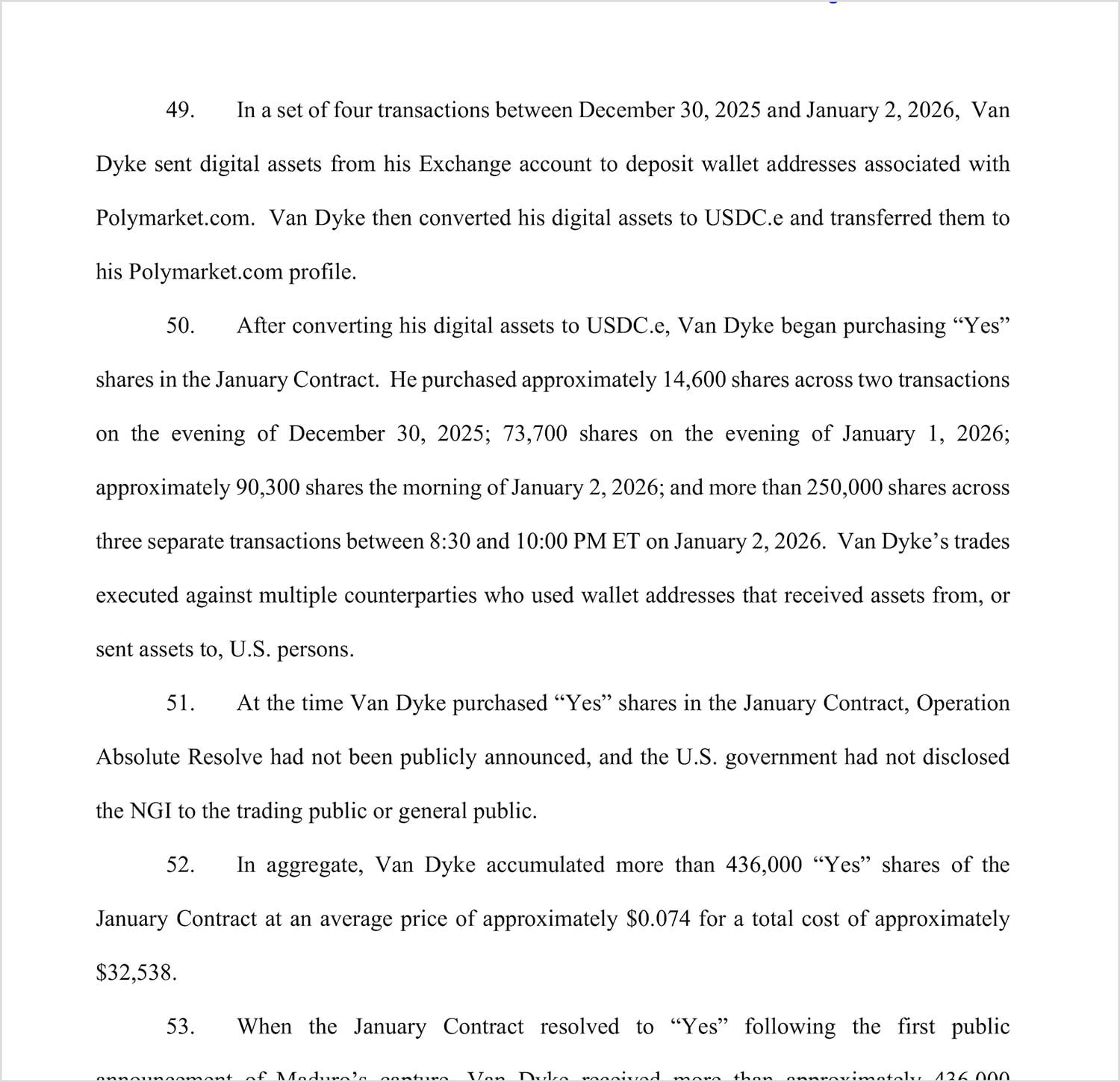

Between December 30, 2025 and January 2, 2026, Van Dyke bought “Yes” shares in the contract titled “Maduro Out by January 31, 2026?” at an average price of seven and a half cents per share. The buying ramped over four nights:

- December 30 evening: 14,600 shares

- January 1 evening: 73,700 shares

- January 2 morning: 90,300 shares

- January 2 between 8:30 PM and 10:00 PM: more than 250,000 shares across three separate transactions

In total: 436,000 shares for $32,538. He had bought more than half his entire position in the ninety-minute window before midnight on January 2. Hours later, U.S. special forces and law enforcement agents captured Maduro and Flores and put them on a plane to the United States.

At 4:21 a.m. Eastern Time on January 3, 2026, President Trump posted on TruthSocial that the operation had succeeded. The contract spiked from $0.375 to $0.955 in four minutes. By 7:14 a.m. it had resolved to Yes. Van Dyke’s $32,538 had become more than $404,000. A 1,200 percent return in roughly four days.

On January 22, 2026, Van Dyke transferred $300,000 of the proceeds from his crypto exchange to his USAA bank account. That single wire transfer became Count Five of his federal indictment, the money laundering charge under 18 USC § 1957.

Three months later, federal prosecutors filed five felony counts against him. The forfeiture allegations target his Interactive Brokers account by number and the $50,066.36 in his USAA Bank account by number. The indictment was signed by Jay Clayton, the former Chairman of the Securities and Exchange Commission and current U.S. Attorney for the Southern District of New York. The CFTC filed a parallel civil enforcement action the same day in the same federal courthouse, asking for a permanent trading ban, disgorgement, civil monetary penalties, and a registration bar.

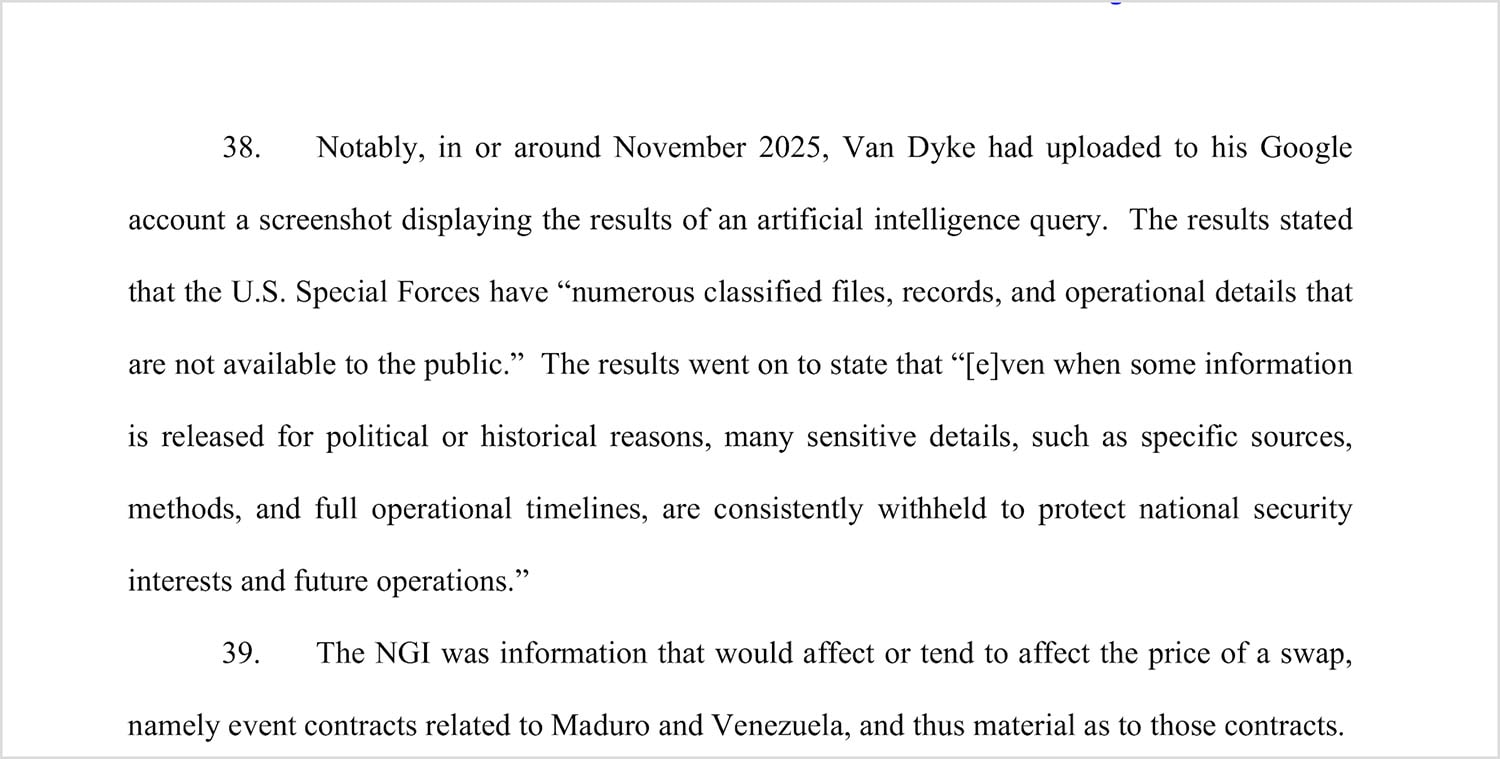

There is one more detail worth pausing on. Two months before any of this trading happened, in November 2025, Van Dyke had used an artificial intelligence tool to ask whether U.S. Special Forces operations are publicly disclosed. He saved a screenshot of the answer to his Google account. The CFTC quoted the screenshot in its complaint:

He researched whether the information was protected. He saved the answer. He traded on it anyway. Federal prosecutors will use that screenshot to argue mens rea at trial. Your search history is evidence. Your AI queries are evidence. The on-chain trail is evidence. The dormant-then-reactivated account is evidence. The dedicated single-purpose wallet is evidence. The Kalshi rejection chats are evidence. None of it disappears.

Watch the full case breakdown

The five federal felony counts

The grand jury returned five counts in United States v. Van Dyke, No. 1:26-cr-00156-MMG. The CFTC also filed civil enforcement charges under three of the same statutory frameworks the same day in CFTC v. Van Dyke, No. 1:26-cv-03369-ALC. Combined maximum criminal exposure: more than 70 years in federal prison plus forfeiture, disgorgement, and civil monetary penalties.

- Count 1, Unlawful Use of Confidential Government Information for Personal Gain under 7 USC § 6c(a)(3) and § 13(a)(5). Often called the Eddie Murphy Rule, after the Trading Places commodity-manipulation scene. Added by Dodd-Frank in 2010 to target federal employees who trade on nonpublic government information. 10-year maximum.

- Count 2, Theft of Nonpublic Government Information under 7 USC § 6c(a)(4)(C) and § 13(a)(5). The companion provision targeting anyone who steals or imparts government information for trading purposes. 10-year maximum.

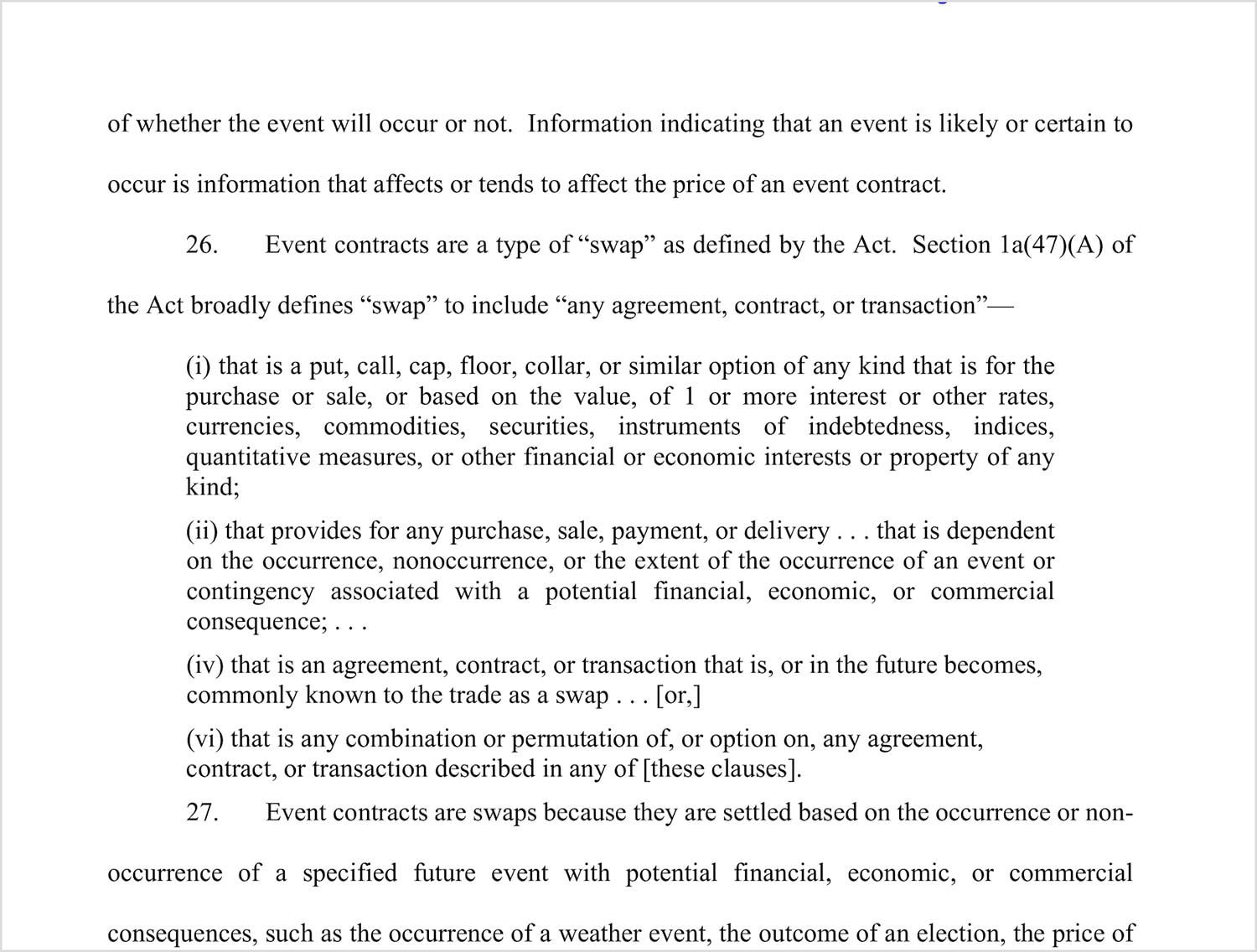

- Count 3, Commodities Fraud under 7 USC § 9(1) and CFTC Regulation 17 CFR § 180.1. The CFTC’s open-ended anti-fraud rule, modeled on SEC Rule 10b-5. Reaches anyone using a manipulative or deceptive device in connection with a swap or commodity contract. 10-year maximum.

- Count 4, Wire Fraud under 18 USC § 1343. The federal anti-fraud workhorse. 20-year maximum.

- Count 5, Money Laundering under 18 USC § 1957. The $300,000 wire transfer to USAA on January 22. 10-year maximum.

Counts 1 and 2 only apply to government employees. Counts 3, 4, and 5 apply to anyone. That distinction is the entire point of this article. The wire fraud and commodities fraud framework that captured Van Dyke captures corporate insiders, lawyers, doctors, journalists, sports insiders, election workers, and anyone else who trades a Polymarket contract on information they had a duty to keep confidential.

What is wire fraud, and why your Polymarket trade may be one

Wire fraud, codified at 18 USC § 1343, is the most flexible federal criminal statute on the books. It applies to any scheme or artifice to defraud, executed using interstate wire communications, where the defendant intended to obtain money or property through false or fraudulent pretenses, representations, or promises. Maximum sentence: twenty years in federal prison per count, thirty if a financial institution is involved, plus restitution and forfeiture.

A Polymarket trade hits every wire-fraud element automatically. The order is routed over the internet, which is interstate wire communication. The trader is trying to obtain money. The only fact question is whether the underlying scheme involves false or fraudulent pretenses. That is where the duty of confidentiality comes in.

Under the Supreme Court’s decision in United States v. O’Hagan, 521 U.S. 642 (1997), trading on confidential information in breach of a duty of trust and confidence to the source of that information is itself a fraudulent scheme. Earlier still, in Carpenter v. United States, 484 U.S. 19 (1987), the Supreme Court upheld wire fraud convictions against a Wall Street Journal reporter who fed his “Heard on the Street” column contents to traders before publication. The reporter was prosecuted for misappropriating his employer’s confidential information. Same theory, different decade. Federal prosecutors call it the misappropriation theory. It does not require that the trader’s counterparty be deceived. It only requires that the trader breached a duty of trust and confidence to the source of the information.

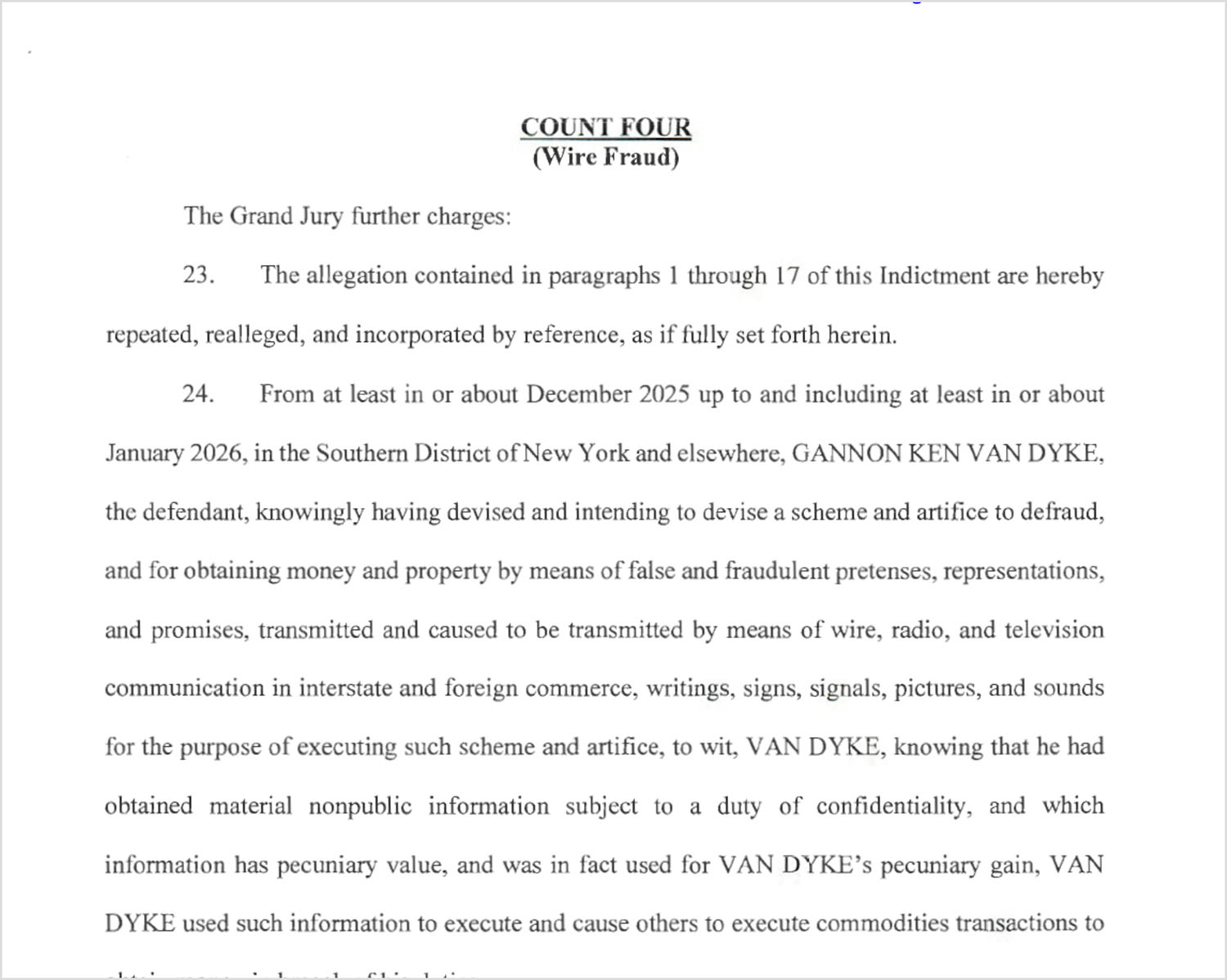

Look at how Count Four of the Van Dyke indictment is pleaded:

That formulation maps directly onto a corporate employee, a lawyer, a doctor, a journalist, a banker, a juror, a referee, a coach, a federal contractor, or anyone else who has a duty of confidentiality to a third party. Substitute “his employer” or “her client” or “his hospital” or “her newspaper” for “the United States Government” in the indictment. The theory is identical. If you have wondered whether what you did is criminal, it is. If you needed an example of how federal prosecutors will charge it, the Van Dyke wire fraud count is your example.

If you are concerned about your own conduct, the most important step you can take right now is to consult with a federal wire fraud defense lawyer before you talk to anyone else, including investigators.

Did I commit a crime? Signs you may be at risk

You are at risk of federal prosecution for Polymarket insider trading or wire fraud if some combination of the following is true.

You traded a Polymarket event contract while you were in possession of material nonpublic information about the event. “Material” means information that would reasonably affect the price of the contract. “Nonpublic” means information that had not been disseminated to the trading public.

You owed a duty of trust and confidence to the source of that information. The duty does not have to be to Polymarket. The duty runs to whoever you got the information from. Under SEC Rule 10b5-2, which the CFTC follows by analogy under Rule 180.1, the relevant duties include any agreement of confidentiality, any history or pattern of sharing confidences, and any spousal, parent-child, or sibling relationship. The duty also arises automatically from employment, attorney-client representation, fiduciary obligations, professional licensing, and security clearances.

You used the information when deciding to enter, exit, or size your position. The government does not have to prove that the trade would not have happened without the information. It only has to prove that you used it.

You traded through a wire transmission, which on Polymarket means the internet. That element is satisfied automatically.

You profited, or attempted to profit. Wire fraud does not require completed gain. Attempted fraud is itself a federal crime under 18 USC § 1349.

If those elements describe your trading, you have potential criminal exposure under 18 USC § 1343 and CFTC Rule 180.1, plus possible exposure under 18 USC § 1348 (securities and commodities fraud, twenty-five-year maximum) and 7 USC § 9(1) (CEA fraud). If you used proceeds from such a trade to make any subsequent transaction over $10,000, you also face potential exposure under 18 USC § 1957 for money laundering, just like Van Dyke does on Count Five.

Stop reading and call a federal criminal defense lawyer if any of those elements are present in your facts.

Why this reaches far beyond government employees

Polymarket lists thousands of event contracts on subjects where ordinary professionals have inside information by virtue of their jobs. The audience for federal exposure is much larger than people realize.

Before walking through the categories of exposed traders, look at the CFTC’s own characterization of these contracts. The agency took the formal litigation position, in a federal pleading, that Polymarket event contracts are swaps under the Commodity Exchange Act:

Now the categories.

Corporate insiders. Polymarket lists contracts on CEO departures, mergers, FDA approvals, earnings beats, IPO timing, and other company-specific events. Any employee, contractor, or vendor with nonpublic knowledge of a coming announcement who trades the contract is in Carpenter territory. Also potentially securities fraud if the underlying company has publicly traded stock.

Lawyers and law firm staff. M&A counsel, criminal defense lawyers with verdict-market knowledge, paralegals who see filings before they hit PACER, IT contractors with access to litigation databases. The duty is the attorney-client privilege and the fiduciary obligation to the client. Federal prosecutors have been bringing these cases against law firm staff for thirty years.

Healthcare insiders. Treating physicians, nurses, hospital administrators, and pharmacy benefit managers who learn nonpublic information about a public figure’s medical condition. Polymarket runs markets on whether named public figures will be hospitalized or will appear at events. A hospital administrator who traded on a patient’s diagnosis has wire fraud and HIPAA exposure under 42 USC § 1320d-6 simultaneously. See healthcare fraud defense.

Sports insiders. Athletes, coaches, trainers, equipment managers, team doctors, referees, and league office personnel. Polymarket has thousands of game and season markets. A trainer who knows the starting quarterback has a concussion and trades the spread is in the same legal position as Van Dyke, with the duty running to the team instead of the Army. The 2024 Jontay Porter NBA prop-bet prosecution was charged on this exact theory.

Anyone bound by a duty of confidentiality. This is the broadest category and absorbs everyone else. Journalists with embargoed news (the original Carpenter fact pattern). Congressional staff and government contractors. Election workers and judicial clerks. Vendor employees, freelancers, consultants under NDAs. Family members under Salman v. United States, 580 U.S. 39 (2016), where information shared in confidence creates fiduciary-equivalent duties. If you owed somebody a duty to keep it secret and you traded on it, you have wire fraud exposure.

If you fit one of these categories and you have traded a Polymarket contract on information you should have kept to yourself, do not assume that the platform’s lack of compliance infrastructure protects you. The Van Dyke case proved exactly the opposite. Kalshi’s compliance system worked. Polymarket’s lack of compliance did not save him. Federal liability attaches because the duty runs to the source of the information, not to the platform.

If you are charged: the defenses your federal lawyer will press

The criminal counts in the Van Dyke indictment are not as airtight as the press release suggests. Three of the five counts depend on a threshold legal question that has never been decided in any criminal case: are Polymarket event contracts actually “swaps” within the meaning of the Commodity Exchange Act?

The strongest defense is that they are not. The statute defines a swap as a contract dependent on an event “associated with a potential financial, economic, or commercial consequence.” That qualifier matters. A traditional swap is an instrument of economic risk transfer: a currency hedge, an interest rate hedge, credit default protection. The trader has a defined economic exposure to the underlying. A Polymarket bet on whether Maduro is captured is not a hedge against any economic exposure of the trader. It is a wager on whether a news event happened. Reading the statute to cover bets on news events drains the qualifying language of meaning, because every event has consequences for someone, somewhere.

The Dodd-Frank Act, which added the event-or-contingency language to the swap definition in 2010, was enacted in direct response to the 2008 financial crisis. Its target was the Wall Street derivatives market that imploded with AIG and Lehman. Polymarket did not exist. Kalshi did not exist. The legislative record contains no evidence that Congress was thinking about consumer betting platforms when it wrote the statute. Stretching the statute to reach retail wagers on news events is the kind of regulatory expansion the Supreme Court has recently held requires clear congressional authorization, not creative agency interpretation.

The rule of lenity reinforces both points in a criminal case. When a criminal statute is genuinely ambiguous, courts construe the ambiguity in favor of the defendant. Section 6c(a)(3), the so-called Eddie Murphy Rule, has sat unused for sixteen years. Van Dyke is the first prosecution. There is no judicial gloss, no settled precedent, and no published guidance reaching DeFi event contracts. That absence is itself a defense.

The wire fraud count, Count Four, does not depend on the swap question and is the count most likely to survive a motion to dismiss. Even there, the defense will press whether the trader actually used the information versus merely possessed it, whether the information was material in light of dozens of other Maduro-related contracts on the market at varying prices, and whether a single trade qualifies as a “scheme to defraud” under federal precedent.

The deeper attack on Count Four runs through three Supreme Court cases that have narrowed federal wire fraud since Carpenter and O’Hagan: Cleveland v. United States (2000), Skilling v. United States (2010), and Kelly v. United States (2020). Each held that wire fraud requires the object of the scheme to be money or property in the conventional sense, and that a sovereign’s regulatory interest in controlling information or licensing is not “property” within the statute. The United States Government’s interest in classified intelligence about Operation Absolute Resolve is sovereign and regulatory, not proprietary. Van Dyke’s scheme was not aimed at obtaining anything from the U.S. Government. He was aimed at Polymarket counterparties, who were not the source of his confidential information and to whom he owed no duty. If the courts apply Cleveland and Kelly to this fact pattern, Count Four falls on the same threshold ground as Counts One through Three. The misconduct may still be punishable through the Espionage Act, 18 USC § 1924, or the Uniform Code of Military Justice. But not as wire fraud.

These are the threshold motions Van Dyke’s lawyers have already told the court they intend to file. The case the press release described as ironclad is closer to genuinely contested. The fact that the government chose Van Dyke as the first publicly charged Polymarket prosecution, on the cleanest possible fact pattern, is itself a tell. They picked the easiest case for the threshold legal questions because they know those questions are vulnerable.

What happens if you receive a federal target letter

A federal target letter is a written notice from a United States Attorney’s Office stating that you are a target or subject of a federal grand jury investigation. Targets and subjects are different categories. A target is a person against whom the prosecutor has substantial evidence linking them to a crime. A subject is a person whose conduct is within the scope of the grand jury’s investigation but against whom the evidence is not yet conclusive.

If a target letter arrives, the worst thing you can do is call the prosecutor or the agent listed on the letter and try to explain yourself. The grand jury is a one-way information gathering machine. Anything you say will be added to the case against you. You have a Fifth Amendment right not to testify, and you have a right to counsel. Use both.

A target letter is also a critical opportunity. It means the government has not yet charged you, and may not yet have decided whether to charge you. A skilled federal defense lawyer can sometimes prevent an indictment by responding to the target letter with a presentation, a proffer, or a defense submission to the prosecutor. That window closes the moment you are indicted.

If you have received a target letter related to Polymarket trading, do not wait. Retain federal counsel immediately. See federal criminal defense in the Northern District of Texas.

What to do if the FBI, CFTC, or SEC contacts you about Polymarket trades

Federal investigations into Polymarket insider trading will come at you from at least three different agencies. The FBI handles wire fraud and money laundering. The CFTC handles commodities fraud and Rule 180.1 violations. The SEC may be involved if the underlying information related to a publicly traded company. The Department of Justice can pursue criminal charges from any of those starting points.

If a federal agent appears at your home or office, contacts you by phone, or sends a letter requesting an interview, the rule is identical for all three agencies. You have the right to remain silent. You have the right to counsel. Use both.

Polite refusal sounds like this: “I am happy to be helpful, but I need to speak to my attorney before I answer any questions. Please leave your card and I will have my lawyer contact you.” That is the entire script. Memorize it.

Do not lie to a federal agent. Lying to a federal agent is itself a federal crime under 18 USC § 1001, with a five-year maximum, even if the underlying conduct turns out not to be criminal. The safer option is always to say nothing until you have counsel.

Do not attempt to delete records, close accounts, or move assets after you learn of an investigation. Each of those acts can be charged as obstruction of justice under 18 USC § 1512, which carries a twenty-year maximum, or as money laundering if assets are moved with intent to conceal under 18 USC § 1956. The forfeiture allegations in the Van Dyke indictment specifically target his Interactive Brokers account and his USAA Bank account by number. The crypto wallet 0x31a5…8ed9 he used on Polymarket is also presumptively traceable. The on-chain trail does not disappear because you stop using the wallet.

Call a federal criminal defense lawyer before you do anything else.

When to hire a wire fraud defense lawyer

The earlier the better. The differences between cases that end in declination, deferred prosecution agreements, plea bargains with reduced exposure, and full indictments often turn on what happened in the weeks and months before charges were filed. A federal defense lawyer who is engaged early can negotiate with the prosecutor, present mitigating evidence, identify constitutional defects in the investigation, and in some cases prevent charges from being filed at all.

Specific moments when you need a wire fraud defense lawyer immediately:

- You receive a federal grand jury subpoena, whether for testimony or documents.

- You receive a federal target letter or subject letter.

- The FBI, CFTC, or SEC contacts you for an interview.

- A federal agent executes a search warrant at your home, office, vehicle, or any other location associated with you.

- You learn that someone you know, traded with, or shared information with has been contacted by federal investigators.

- You have any reason to believe you may be under federal investigation, even before any of the above has happened.

The retention itself is privileged. The fact that you talked to a federal defense lawyer does not appear in any government record. The conversations you have with your federal defense lawyer are protected by attorney-client privilege and cannot be used against you.

Federal white collar criminal defense in the Northern District of Texas

I represent clients in federal criminal investigations and prosecutions throughout the Northern District of Texas, the Eastern District of Texas, and on a case-by-case basis throughout the United States. My practice covers the full spectrum of federal white collar offenses, including wire fraud, mail fraud, securities fraud, commodities fraud, healthcare fraud, money laundering, conspiracy, obstruction of justice, and tax fraud, alongside federal drug, weapons, and violent crime cases.

I am board certified in criminal law by the Texas Board of Legal Specialization, which fewer than two percent of Texas lawyers achieve. I am a former Dallas County felony prosecutor. I have tried more than 150 jury trials. I know how the federal criminal system actually works in Dallas, Fort Worth, Plano, Sherman, Tyler, Marshall, Beaumont, and Houston.

If you need any additional confirmation of how seriously the federal government takes Polymarket insider trading, look at who personally signed the Van Dyke indictment:

If the analysis above describes your situation, or if you simply want a confidential, privileged conversation about whether you have exposure, the next step is calling my office.

Law Offices of Michael Lowe

700 N. Pearl Street, Suite 2170

Dallas, Texas 75201

Telephone: 214-526-1900

Email: mlowe@dallasjustice.com

The conversation is confidential and there is no charge for the initial consultation.

____________________________________________________________

This article is for general informational purposes. Reading it does not create an attorney-client relationship. The Van Dyke prosecution is at the indictment stage, and Mr. Van Dyke is presumed innocent unless and until proven guilty in a court of law. Nothing in this article should be construed as a comment on Mr. Van Dyke’s guilt or innocence. The general legal analysis applies to anyone considering or evaluating Polymarket-related criminal exposure under federal law and is not specific legal advice for any particular reader. If you have facts you want analyzed, retain counsel for a confidential, privileged consultation.

Comments are welcomed here and I will respond to you -- but please, no requests for personal legal advice here and nothing that's promoting your business or product. Comments are moderated and these will not be published.

Leave a Reply